Many students will soon begin their first year at university in the near future.

For many, handling their student loans will be their initial experience with financial autonomy.

However, being a student carries a significant financial burden, with nine out of ten university students reporting feelings of being overwhelmed when it comes to handling their money, according to Visa's research.

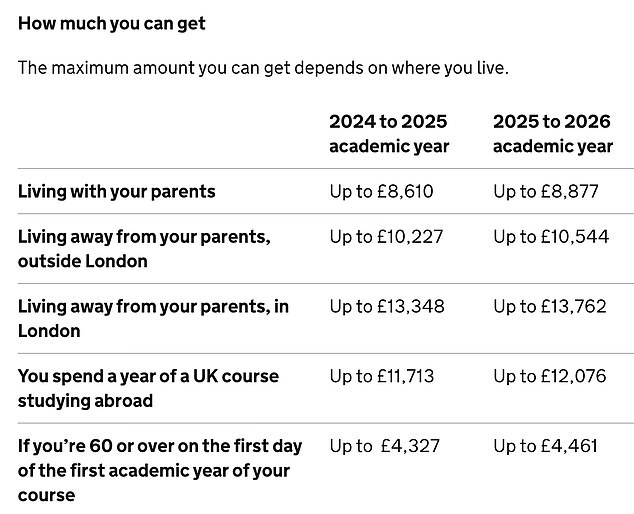

Tuition costs for an undergraduate program in England can go as high as £9,535 annually, while the highest maintenance loan available for students studying away from home outside London is £10,544. This means a three-year degree might exceed £60,000 in total.

In this section, we examine ways to manage and organize your financial affairs if you're about to start university.

How student loans work

A student loan consists of two components: the tuition fee loan and the living expenses loan.

Most university students are eligible for a student loan, which is currently limited to £9,535 per year.

This amount is paid directly to the university by Student Finance — a collaboration between the Government and the Student Loans Company, which manages the student loan program.

Maintenance loans intended to cover living expenses are deposited directly into students' bank accounts. For the 2025-26 academic year, students studying in England are eligible for a standard maintenance loan of £4,915 without needing to provide information about their household income.

Students whose family household income is approximately £62,350 or lower might qualify for a larger maintenance loan, which means their parents will need to supply income information.

When is it time to repay a student loan?

They begin repaying their student loan after they start earning above a specific threshold.

Unlike a typical loan, the system functions more like a graduate tax and increases as your income rises. The amount you repay and the method depend on which of the five distinct repayment plans you are enrolled in.

The majority of students beginning university this year, as well as those who started their studies after September 1, 2023, are enrolled in Plan 5. This implies that they will begin repaying their loans once their income exceeds £25,000.

In Scotland, however, students are under Plan 4 and will begin repaying the loan once their annual income exceeds £32,745.

Individuals enrolled in Plan 2 who attended university between September 1, 2012, and July 31, 2023, will begin repaying their loan when their income exceeds £28,470.

Individuals who enrolled in university prior to September 1, 2012, are under Plan 1 and will begin repaying their loan when their annual income exceeds £26,056.

Every graduate, no matter which plan they are enrolled in, pays 9 percent of their income above the threshold, whereas individuals with postgraduate loans pay 6 percent.

The period before unpaid debt is forgiven was extended from 30 years to 40 years. This is expected to result in more graduates repaying their loans entirely.

What is the cost associated with student loans?

Student loans begin to accumulate interest from the moment you enroll in your program and keep adding up until the loan is fully repaid. The interest rate you are charged is determined by the government and may vary annually.

The rate of interest charged on student loans isAccording to the current Retail Price Index inflation rate of 3.2 percent.

However, when the RPI reached 13.5 percent in March 2023, the Government imposed a limit of 7.6 percent on all student loans.

Students enrolling at university this year will be part of Student Loan Plan 5. The interest rate for the period beginning on 1 September 2025 will be 3.2 percent.

The present level of interest in the other plans is as follows:

Plan 1: 3.2 percent

Plan 2: 3.2 percent to 6.2 percent, based on income

Plan 4: 3.2 percent

Postgraduate loans: 3.2 percent to 6.2 percent, based on earnings

For Plans 2 and 5 loans, individuals with an income below £26,900 are charged the RPI interest rate, whereas those earning between £26,900 and £39,130 pay the RPI rate plus up to 3 percent, with the additional percentage increasing as your income rises.

Individuals with income exceeding £51,245 are subject to RPI plus an additional 3 percent.

How to create a budget

It's well-known that numerous students operate on a very limited budget. Nonetheless, creating a weekly or semester budget can simplify handling your finances.

Initially, determine your necessary expenses, such as rent, study supplies, utility costs, groceries, and commuting - everything you absolutely cannot do without.

After you have added them all together, you can subtract that total from the amount of money you have available, which may include your loan, scholarships, income, or gifts from relatives.

For students, it often makes sense to analyze expenses on a term-by-term basis and then establish a weekly budget with spending caps," says Laura Suter, director of personal finance at AJ Bell. "This helps you monitor your spending – if you go over a bit one week, you can adjust slightly the following week.

Once you've completed this, you'll have a clearer understanding of what remains to be done for other aspects, such as socializing, purchasing new clothing, and engaging in hobbies and interests.

A useful suggestion is to transfer each payment of your maintenance loan into a separate account immediately upon receiving it, and then replenish your current account with your weekly expenses at the beginning of every week.

You will be given the maintenance loan in three payments per year, which helps minimize the chance of unintentional overspending.

Certain students promptly move enough funds to cover bills and rent for the entire three-month period into a distinct account, ensuring they are never tempted to use money designated for necessities.

Budgeting tools and organizers designed for students are available on the websites Save the Student and UCAS.

Understanding overdrafts

A key attraction of a student current account is the significant interest-free overdraft facilities included.

This basically enables you to access funds from your existing account without any charges.

This offers a significant advantage, considering the high interest rates applied to non-student accounts. With a regular bank account, you might be charged between 35% and 40% for an agreed overdraft — this translates to £350 to £400 in interest over 12 months if you have a £1,000 overdraft on your current account. If you're borrowing £3,000, the annual interest would range from £1,050 to £1,200.

However, it is crucial to use your overdraft only for necessary expenses when there are no other alternatives. It is also highly inadvisable to exceed the agreed-upon limit.

Overdrafts must be repaid, and the 0 percent interest promotion typically stops after you finish school—so you wouldn't want to have a large amount of debt to settle at that point.

Several choices are available for students looking to open an account this year.

Santander offers a student account that includes an interest-free overdraft of £1,500 during the first three years of study. The limit can be increased to £1,800 in the fourth year and up to £2,000 if students continue into their fifth year.

Nationwide's current account provides interest-free and fee-free overdrafts for students, reaching up to £3,000 by their third year.

NatWest and RBS provide accounts that include a £500 interest-free overdraft during the first term of the first year, which can be increased to £2,000 in the second term of the first year until the end of the second year. From the third year onward, students may apply for up to £3,250 in interest-free overdraft.

In the meantime, HSBC's student account offers a £1,000 interest-free overdraft during the first year, which rises to £2,000 in the second year, and reaches £3,000 from the third year onward.

Rachel Springall, from the comparison site Moneyfacts Compare, states: "The most favorable overdrafts are offered by NatWest, HSBC, and Nationwide Building Society, which can serve as a crucial financial support for students requiring funds during their studies."

Nevertheless, engaging in some part-time employment during their studies to gain a little extra money is prudent, as an overdraft must eventually be repaid.

Sarah Coles from stockbroker Hargreaves Lansdown states: "You must be very clear that this is solely for necessary expenses when absolutely required—and you should never exceed your set limit."

When you finish school, you'll need to repay it fairly soon, so avoid creating difficulties for yourself.

The amount of your overdraft in future years will be determined by your credit history, and you must request any increases at the end of the year, as they are not automatically granted.

No comments:

Post a Comment